New renderings have been revealed for Gowanus Green, a six-building mixed-use complex in Gowanus, Brooklyn. Designed by Marvel Architects and developed by The Hudson Companies, Jonathan Rose Companies, The Bluestone Organization, and Fifth Avenue Committee, the four-acre master plan will yield 990,000 square feet across six buildings with 950 affordable homes, retail and community space, an 80,000-square-foot public grade school, and a new waterfront esplanade. SCAPE is the landscape architect for the project, which is bound by 5th Street to the northeast, Smith Street to the northwest, the Gowanus Canal to the southeast, and a vacant plot at 459 Smith Street to the southwest.

The aerial rendering above shows the structures enclosed in red and earth-toned brick façades surrounding orderly grids of large windows. Setbacks across multiple structures and their parapets are shown topped with green roofs, along with several photovoltaic arrays. A new tree-lined street is depicted cutting through the development, running from Smith Street to a central cul-de-sac. The tallest tower in the complex appears to stand 28 stories high.

The following renderings give a closer view of the retail and community spaces at street level, as well as the buildings’ brick façades and fenestrations with dark metal frames and spandrels. Glass railings line some of the rooftops and setbacks, and canopies mark the location of some of the residential entrances. New street lamps and garden beds will also surround the walkways.

Affordable homes at Gowanus Green will cater to a wide range of incomes and needs, including formally homeless, seniors, and low-income New Yorkers. Community spaces are slated to provide early childcare, healthcare, senior programming, and space for artists.

The nearest subways from the development are the F and G trains at the Smith-9th Streets station to the south and the Carroll Street station to the north.

A start and completion date for Gowanus Green has yet to be finalized.

New renderings have been revealed for 520 Fifth Avenue, a 1,000-foot residential supertall skyscraper under construction in Midtown, Manhattan. Designed by Kohn Pedersen Fox and developed by Rabina, which took over from Ceruzzi Properties and SMI USA in 2019, the 76-story structure will span 415,000 square feet and yield 98 condominium units and commercial space spread across the ground floor and four cellar levels. WSP is the structural engineer, DeSimone Consulting Engineers is the façade consultant, and Suffolk Construction is the general contractor for the property, which is located at the northwest corner of Fifth Avenue and West 43rd Street, one block north of Bryant Park.

The collection of renderings from Binyan Studios showcases the upper levels and crown, ground floor, and lower setbacks in greater detail than previous depictions. The main photo above previews the top of the skyscraper’s northern elevation, on which the arched window motif stretches to enclose the tower up to its pinnacle. This image also reveals a terrace atop the shallow setback on the narrow eastern face near the top of the structure. At these levels, residents will have dramatic views of the surrounding Midtown skyline and the Empire State Building and World Trade Center to the south.

520 Fifth Avenue. Rendering courtesy of Binyan Studios

The second rendering looks down at the ground-floor entrance, highlighting the details in the arched columns and façade. The building’s address is shown embedded into the sidewalk in interlocking numerals at the foot of the main doors.

520 Fifth Avenue. Rendering courtesy of Binyan Studios

The third and fourth renderings offer a glimpse into the skyscraper’s interiors through its arched floor-to-ceiling windows, as well as a closer perspective of the glass-lined terraces atop the setbacks.

520 Fifth Avenue. Rendering courtesy of Binyan Studios

520 Fifth Avenue. Rendering courtesy of Binyan Studios

“Our design for the 520 Fifth Avenue tower combines the setbacks of Hugh Ferris’ 1920s New York with arches arranged in modular bundles, rising to 1,000 feet,” said James von Klemperer, KPF president and design principal for the project. “The architectural expression of stepping volumes echoes the setbacks of midtown towers, while the delicately articulated exterior wall details are inspired by the façade of The Century Association adjacent to our site. We also looked to the arches of the landmarks in the neighborhood, including the New York Public Library and Grand Central Terminal, translating these forms into a modern version of this motif.”

Construction has continued to ascend since our last update a month ago. Recent photographs show the skyscraper nearing the one-third mark, followed closely behind by the installation of the prewar-inspired façade.

Photo by Michael Young

Photo by Michael Young

Photo by Michael Young

Photo by Michael Young

The nearest subways from the development are the B, D, F, M, and 7 trains at the 42nd Street-Bryant Park/Fifth Avenue station. The property is also in close proximity to the Grand Central-42nd Street station, serviced by the 4, 5, 6, 7, and Shuttle trains, as well as Metro-North and Long Island Rail Road trains at Grand Central Terminal and Grand Central Madison.

520 Fifth Avenue’s completion date is posted on the construction board for June 1, 2026.

Under the new 11-year lease agreement, which was announced by Irvine Company and Tishman Speyer, MetLife will maintain its substantial footprint in the building, occupying the entire third and sixth floors, along with parts of the mezzanine, fourth, and fifth floors. The company initially consolidated its New York City offices to the 58-story tower in 2017.

200 Park Avenue, co-owned by Irvine Company and Tishman Speyer, has undergone a substantial renovation to rejuvenate its 3.1 million square feet of space. Upgrades include lobby renovations, enhanced connection to Grand Central Terminal, new outdoor gardens and customer lounges, a fitness center, and event spaces.

Currently, the MetLife Building is 96 percent occupied, with over 800,000 square feet of new leases, extensions, and renewals since 2020. Designed by Pietro Belluschi, Walter Gropius, and Emery Roth & Sons in the International style, 200 Park Avenue first opened in 1963 as the Pan Am Building. MetLife acquired it in 1980 and added its logo to the top in 1993. Tishman Speyer and Irvine Company have been the owners since 2005, with MetLife retaining naming and signage rights.

The lease extension was facilitated by Tishman Speyer’s Megan Sheehan and Sam Brodsky, representing the co-owners, while a Cushman & Wakefield team led by Patrick Murphy and Peyton Horn represented MetLife.

“MetLife’s continued presence at 200 Park Avenue is a testament to the connection between the iconic building and one of the world’s leading financial institutions,” said Roger DeWames, division executive vice president, Irvine Company Office. “We are proud to extend our partnership with MetLife as the next chapter of 200 Park begins.”

CIM Group hands back keys to NY building, SF building loses 84% of value due to coworking firm’s travails

RFR’s Aby Rosen and Kushner Company’s Laurent Morali and Nicole Kushner Meyer with a WeWork office (Illustration by The Real Deal with Getty, Kushner)

OCT 21, 2023, 7:00 AM

By

Ted Glanzer

Nowhere is office distress more evident than with WeWork, which, despite its name, isn’t working at all.

Indeed, the coworking firm could be renamed “ReWork” after its staggering losses have forced it to renegotiate nearly all of its leases.

Landlords that count WeWork as a top five tenant owe about $2.6 billion in CMBS debt, an analysis of Trepp data shows. About half of those loans come due within 12 months and nearly 80 percent are either watchlisted, delinquent or in default.

Kushner Companies and Aby Rosen’s RFR are already weathering the fallout of a WeWork departure. The landlords failed to refinance their Dumbo office complex and landed in maturity default last month. WeWork had ditched a majority leasehold in one of the portfolio’s four buildings.

The Los Angeles–based landlord, which picked up the large office property with Australian pension fund QSuper in 2017, saw the $399 million loan backed by the Midtown building go to special servicing this month, according to Trepp.

“The special servicer comments are not encouraging,” a Trepp email alert reads, noting that WeWork, which had been the building’s top lessee, has vanished from the tenant list. A WeWork spokesperson said the firm is still a tenant at 1440 Broadway and a change in building ownership would not affect that.

The CMBS loan had gone to a special servicer because “there is no single lender to negotiate with and the loan must first be transferred to special servicing in order to enter into any negotiations,” CIM said in a statement.

Sellers barely north of breakeven on Hiroshi Sugimoto–designed apartment

432 Park Avenue (Getty)

OCT 23, 2023, 2:45 PMUPDATED OCT 23, 2023, 5:00 PM

By

Harrison Connery

After two years on the market, the 79th floor unit at 432 Park Avenue has sold for less than half its original asking price.

The 8,000-square-foot apartment at the Macklowe-CIM supertall sold to an unknown buyer for $65.6 million, according to property records, after having hit the market two years ago with an asking price of $135 million. Two studio units were also sold separately as part of the deal, bringing the total transaction price to $70 million.

The asking price was lowered in May to $92 million and went into contract in August. The sale price is roughly what the sellers paid for the apartment in 2016.

Listing agent Noel Berk of Engel & Volkers declined to comment, but previously told The Real Dealthe unit was being marketed to Asian buyers returning to the city post-pandemic.

The 79th-floor unit was designed by Japanese architect Hiroshi Sugimoto, who imported weather-beaten stones from Kyoto and old growth Canadian Hinoki Cypress wood. The five-bedroom, five-bathroom home also has a tea room and bonsai plant sculpture.

The sellers, who have hidden their identity behind a shell corporation, aren’t the first in the building to reconsider their asking price. It is unclear whether the reductions are attributable to initially aspirational pricing, a high-profile lawsuit alleging condo defects, fatigue in the ultra-luxury market or other factors.

In the lawsuit, the condo’s board blamed developers CIM and Macklowe Properties for flooding, eerie noises and an electrical explosion.

Saudi retail magnet Fawaz Alokair listed his top-floor penthouse for $170 million in 2021, then pulled it off the market before relisting it last year for $130 million, according to Streeteasy. The owners of an 84th floor unit who paid $21.4 million in 2016 have cut their asking price to $15 million from the $18 million they sought in February.

Another drama at the controversial building pits its development partners, CIM and Macklowe Properties CEO Harry Macklowe, against each other. CIM wants to foreclose on Macklowe’s personal residences in the building, accusing him of defaulting on $46 million in loans it gave him for three units.

Macklowe says CIM swindled him out of $110 million in distributions he’s owed as a developer. This month he delayed a foreclosure auction on his units by putting them in bankruptcy protection.

Editors Note: We wanted to bring attention to a friend and business associate Dean Marchetto. A relevant force and promoter of Jersey City and all the design standards he has worked to instill and enforce in our way of architectural progress in Jersey City. Dean has remained consistently professional, forward thinking and a proponent of the highest values of his profession. To our friend, Congratulations!

Pictured: Dean Marchetto and Michael Higgins

AUG 28, 2023, 10:00 AM

By Brand Studio

Jersey City has always had a great view of the Manhattan skyline, but in the last 15 to 20 years, the city across the Hudson River has developed an impressive skyline of its own. Dean Marchetto is the founding principal of MHS Architecture, an award-winning architectural firm with a strong focus on urban planning and design. The firm, formerly known as Marchetto Higgins Stieve, has been based in Hoboken for more than 40 years.

Marchetto and Michael Higgins, Managing Principal at MHS Architecture, spoke with The Real Deal about the increasing number of high-rise developments in Jersey City — and how they’ve adapted to meet developers’ changing needs.

“Up until maybe 20 years ago, New Jersey didn’t have much of a high-rise development market, so there were very few architects that had experience with high-rise development,” says Marchetto. “Being here for the past 40 years enabled us to gain that experience. Now, after getting a dozen or so of those buildings built, we’re experts. We’ve become the high-rise guys in New Jersey.”

270 Johnston

Development that originated along the Jersey City waterfront has spread to nearby neighborhoods including Journal Square and Bergen-Lafayette. Higgins notes that the MHS project 270 Johnston, a new mixed-use 24-story residential tower in Bergen-Lafayette, is now the tallest building in that area.

With a planned $100+ million renovation of the historic Loew’s Jersey Theatre, and the Centre Pompidou x Jersey City scheduled to open in 2026, the city is primed for a cultural renaissance. Higgins says, “The biggest change is that Jersey City was once a bedroom community for New York, and now with these cultural institutions getting constructed, it’s becoming more of a thriving metropolis.”

Developers view Jersey City as a great place to invest, and Higgins believes the city’s mayor deserves credit for that. He says, “Steve Fulop has provided excellent leadership over the past decade, and it’s really transformed the city, including not just the high-priced downtown waterfront neighborhoods, but all the neighborhoods in the entire city.”

Mayor Fulop speaks highly of MHS as well. “Marchetto Higgins Stieve Architects have been essential to the growth and development of Jersey City,” he says, explaining, “They were engaged in collaboration with our Planning Department long before most developers believed the growth was even possible. They have had a hand in much of the progress over the last 25 years here in Jersey City and are extremely well respected.”

A Wealth of Local Knowledge and Relationships

Jersey City has seen an influx of New York developers, and it’s common for them to seek guidance from locals as they navigate the challenges of working in a different state. Higgins says, “The New Jersey market is different than the New York market, but that’s where our local knowledge of the market trends, local codes, and everything else comes into play and adds value to the project.”

For example, residents along the New Jersey waterfront love their Manhattan views. With each new project, the MHS architects make those views a priority. Typically, when a tower is built, only one side has the preferred view. In comparison, a stepped design extends each apartment further out as you move back in the building, giving three sides great views of New York City and the Hudson River. “You create value when you create views. Many of our plans are oriented around creating views and doing it with a simple elegance that appears effortless and beautiful,” says Marchetto.

From the beginning, MHS has focused its work on urban areas of New Jersey.

“We’re urbanists,” Higgins explains, “We focus on transit-oriented developments, downtown development, and placemaking. We do everything from building design to urban design and urban planning.”

Both Dean Marchetto and Michael Higgins reside locally — Marchetto has lived in the area his whole life, while Higgins has been there 30 years. They understand the urban landscape not just on a professional level, but also a personal one. This makes it easy for them to communicate its appeal, including walking to restaurants and the light rail, to developers looking to attract buyers and leasers. Marchetto says, “Living the urban experience in this area allows us to advise our clients better.”

The Hendrix

MHS clients also benefit from the team’s long-standing relationships with members of the local community, including zoning and planning officials, the building department, consultants, contractors, and neighborhood groups. Because of its vast local network, MHS is often asked to recommend land-use attorneys, civil engineers, and other industry professionals.

Marchetto says, “We’re able to advise our clients on assembling the best team of professionals for a particular project or location, and who has the best rapport and relationships. Developers need guidance when they’re working in a new area, and we’re happy to help.”

The firm’s extensive experience working in New Jersey gives them a deep familiarity with the entitlements process. When developers want to build in Jersey City, Newark, Bayonne, or Hoboken, they typically want to build as big of a building as they can get approved on their property. Knowing the approvals process and zoning precedents helps MHS position its clients in front of municipal boards in the most favorable and effective way.

For example, they recently worked with three developers — the Albanese Group, Silverman Neighborhoods, and Liberty Harbor Development — on a Jersey City project called the Hendrix, a 40-story structure with about 482 residential units, a state-of-the-art black box theater, and an art center. Marchetto says, “The zoning for that area allowed a 40-story building because of a zoning bonus for the give-back to the arts.”

When the units in the Hendrix went up for lease, they went so fast that the website had to be shut down temporarily. As the national housing shortage continues, Marchetto believes that Jersey City is in a great position to use that as an incentive for further development of the city, its infrastructure, and its placemaking.

Guiding the Redevelopment of Journal Square

As MHS earned a reputation for doing great work, the firm’s projects have grown in size. The Journal Square Redevelopment Plan, MHS’s largest project to date, is also one of the biggest single development areas in New Jersey history. Journal Square was once the historic center of Jersey City, but it was left behind when the waterfront took off during the mid-1970s. In order to reinvigorate the 244-acre area, the city’s previous administration and the Jersey City Redevelopment Agency, headed up by then-director Bob Antonicello, initiated a redevelopment process.

MHS, working alongside renowned planner Tony Nelessen got the contract and produced a vision plan encouraging a comprehensive development that includes walkability, sustainability, transit-oriented design, and putting density where transit is in order to reduce dependence on the automobile. Their plan became the Journal Square 2060 Redevelopment Plan and legal zoning document for the entire district.

Today, Journal Square developers feel like the sky’s the limit — and as it turns out, that’s relatively accurate. Marchetto shares, “It’s probably the only plan I’ve ever seen where the height limit is unlimited. If you look in the zoning, there’s no height restriction in the city’s central core, so you can build as high as the Federal Aviation Authority will allow you to build.”

425 Summit Ave.

When developers looking to build in Journal Square need architectural services, they often reach out to the authors of the plan.

Marchetto says, “Combining our architectural experience with the planning knowledge gives us a unique advantage.”

MHS is working with Eliot Spitzer on the development of 425 Summit Ave, a high-rise mixed-use multifamily development in Journal Square. It’s Spitzer’s first development project in Jersey City, and he appreciated the company’s guidance. He says, “MHS was superb in so many ways — their sense of aesthetics is wonderful, their understanding of Jersey City unrivaled, and their ability to navigate the local entitlement process unmatched. I could not have been happier in every way in our relationship.”

After working locally for more than 40 years, the MHS Architecture team has comprehensive knowledge of every aspect of the process. “There is no substitute for experience when it comes to getting things done,” Marchetto says. “In the past when New York developers came into New Jersey they brought their own architects. Today that is no longer necessary. MHS offers the same creativity and depth of service, along with the local expertise needed to maximize the profitability of your project.”

Generous tenant-improvement packages left cash flows thin when remote work and higher interest rates hit

AUG 7, 2023, 7:00 AM

By

Rich Bockmann

As offices started transforming in the mid 2010s from drop ceilings and cheap carpet to resemble mid-century styled hotels packed with amenities like ping-pong tables and fully-stocked bars, the real estate team at insurance giant Prudential had an epiphany.

All the cash landlords were giving tenants to build out those pricey spaces was eating into the bottom line.

“It became clear to us that the dynamics of office had permanently changed,” said Lee Menifee, head of research for the Americas at PGIM Real Estate.

The writing was on the wall for PGIM and others who could see that offices would struggle. Around 2015 the insurer began shifting the bulk of its real estate portfolio away from workplaces and toward property types with better prospects, such as apartments and warehouses.

“Some investors started to sell down their office assets,” he added. “I think we were a little earlier.”

While the existential threat offices are dealing with now has largely been blamed on remote work and higher interest rates, the truth is that the sector had been struggling with disappointing returns for roughly a decade before Covid hit.

Had office buildings not seen their cash flows eaten away by those ever-climbing expenses, they arguably would have been in a better position to cope with the one-two punch of sinking demand and rising borrowing costs.

Offices in the country’s 20 largest central business districts saw returns underperform in all but two years since 2008, according to data from the National Council of Real Estate Investment Fiduciaries.

Part of this had to do with the outsized gains seen in areas like industrial and multifamily properties. But a driving factor was the escalating costs it took to attract tenants in the form of free rent and tenant improvement allowances.

Sign Up for the National Weekly Newsletter

SIGN UP

By signing up, you agree to TheRealDeal Terms of Use and acknowledge the data practices in our Privacy Policy.

Concessions like these typically tick up in soft markets when there’s more competition to land tenants. This time around, though, they became sticky as markets recovered following the Great Recession.

Office owners started dangling more sweeteners to lure companies to their buildings. Tenants began relocating offices more often than they had in the past, creating an incentive spiral that got out of hand.

“Long before the pandemic, we were seeing that tenants wanted more flexibility and highly-amenitized spaces, which resulted in office capital expenditure requirements increasing faster than rents,” said a spokesperson for Blackstone Group.

The firm, like PGIM, decided to reduce its focus on offices, which in 2007 made up roughly 60 percent of its portfolio. That share has shrunk to less than 2 percent today.

How significant are these costs to a building’s operations? When the total outlay for free-rent periods and tenant-improvement packages are factored in, it can be three to five years into a lease before a landlord starts to make money on the deal.

And the bad news for building owners is that those costs don’t seem to be softenting any time soon.

Tenant allowances went from about $67.50 in 2019 to more than $95 at the start of 2023, according to CBRE. Free rent went from roughly 7 months to more than 10.

And with interest rates going up, it’s going to cost even more to write those TI checks, according to CBRE’s Julie Whelan.

“It’s become much more expensive for landlords to give these allowances,” Whelan said.

Developers built the city up despite rising interest rates, empty offices and a major multifamily policy loss.

From left: Domain Companies’ Matt Schwartz, Joseph Chetrit, Extell Development’ s Gary Barnett and Taconic Partners’ Charles Bendit and Paul Pariser (Photo-illustration by Kevin Rebong/The Real Deal; photos via Getty Images, Domain Companies, Taconic Partners)

JUL 3, 2023, 7:00 AM

By Ellie Quilan Houghtaling

Research by Matthew Elo

Uncertainty reigns in real estate, but New York City developers are still reaching for the sky.

The city’s biggest builders have spent the past year shackled by rising interest rates, persistent supply-chain issues, a battered office market and a murky future for multifamily projects without the popular 421a tax break.

Despite all of this, developers came out of the year predicting gains in a down market and a cheery outlook for the city’s resilience as it continues to recover from the pandemic.

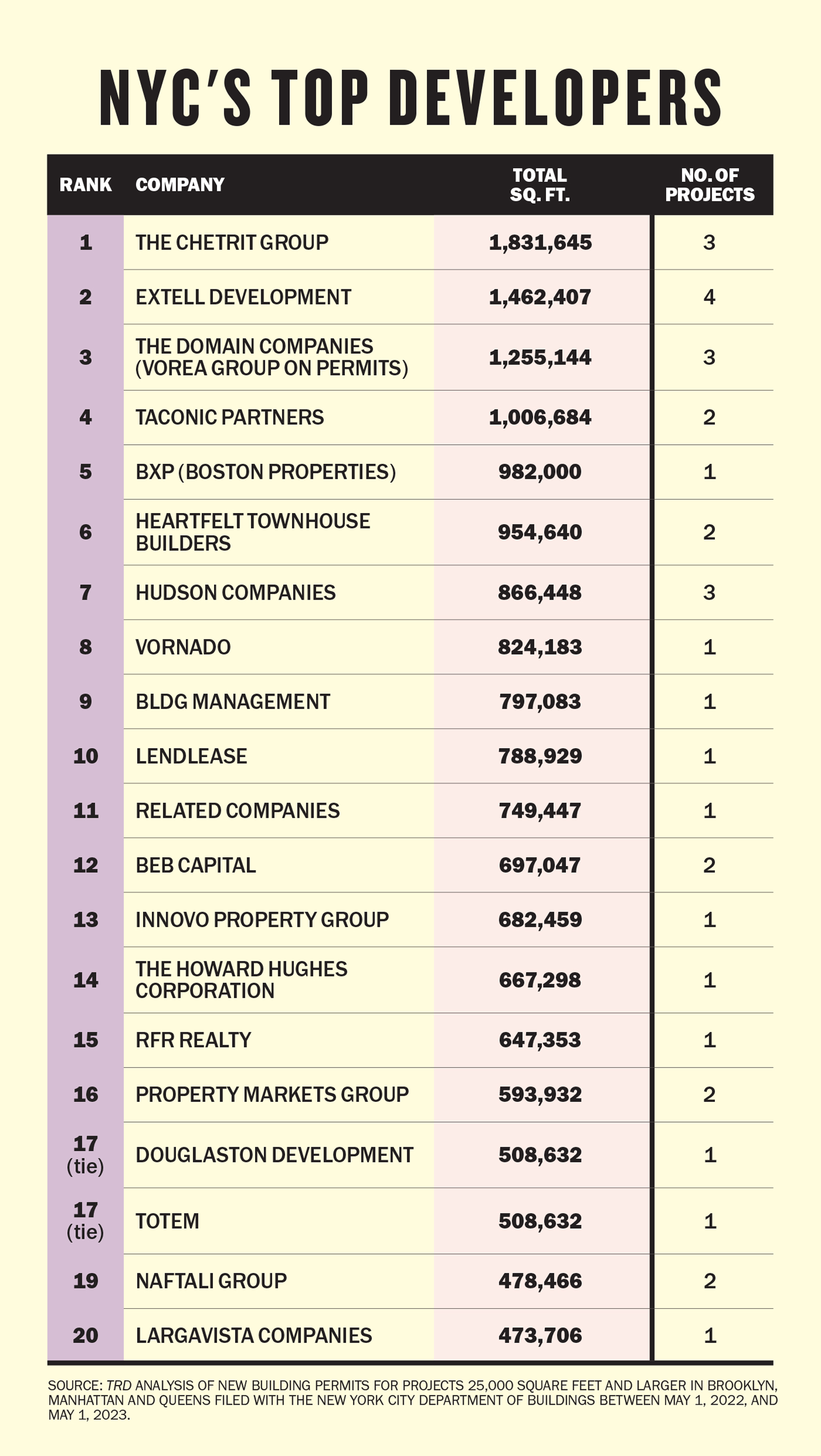

In the 12 months preceding May 1, the city’s 20 most active developers filed plans for 16.7 million square feet of new development — nearly a million more than in the previous year-long period.

To gain a clearer picture of which developers have the most skin in the game in the coming years, The Real Deal analyzed all new building filings submitted to the Department of Buildings between May 1, 2022, and May 1, 2023.

For the second year in a row, Moroccan émigré Joseph Chetrit’s eponymous firm topped the list, filing plans to develop just shy of 2 million square feet across three new projects. Its plans included the largest filing in the city: a 71-story mixed-use skyscraper with allotments for affordable housing on a Two Bridges development site that Chetrit Group bought from CIM Group and L+M Development Partners for $100 million in 2021.

Also included in the firm’s count is 100 West 37th Street in the Garment District, where Chetrit filed plans for a 360,000-square-foot, 68-story tower.

Gary Barnett’s Extell Development placed second, plotting out four new developments that combine for an estimated 1.5 million square feet. Extell’s major projects include 259 Clinton Street, a 421a-approved, 62-story tower just a block from Chetrit’s Two Bridges site. On the Upper East Side, Barnett’s firm filed more plans for a 30-story, 400,000-square-foot medical tower at 403 East 79th Street, also known as 1520 First Avenue.

Rounding out the top three was Domain Companies, which filed plans for nearly 1.3 million square feet across three multifamily projects. Those included a 500-unit complex at 2-33 50th Avenue in Long Island City and two Gowanus projects: a 360-unit, two-tower development at 420 Carroll Street and a 241-unit building at 545 Sackett Street.

Multifamily limbo

The end of 421a last summer created a host of challenges for developers. For those who managed to get foundations laid in time to qualify for the tax break, the 2026 construction deadline now looms large. Some worksites across the city could face supply-chain hiccups that could have a devastating effect.

“I think it’s at the point now where the deadline is getting a little bit close for comfort,” said Domain Companies co-founder Matt Schwartz.

Hopes fluttered and then faltered over Gov. Kathy Hochul’s housing plan, which sought to address some of these challenges but failed to garner enough support from state lawmakers. Entering summer without an immediate replacement for 421a in the cards, developers say they’re focusing on projects already in their portfolio rather than reaching for the horizon.

“If we don’t have something in the pipeline and advancing, we’re generally stuck in a kind of wait-and-see mode. Which is unfortunate, given where we are,” Schwartz said. “We’re very bullish on New York, but the affordability crisis is a real threat.”

“Those that aren’t prepared to proceed to hit the deadline are going to be hurt,” added Lee Brodsky, CEO of BEB Capital, which placed 12th on the list with nearly 700,000 square feet across two projects.

Developers who find themselves unable to meet the deadline will have to find other solutions for their overpriced land, with possible pivots toward condos or luxury rentals.

Sign Up for the National Weekly Newsletter

SIGN UP

By signing up, you agree to TheRealDeal Terms of Use and acknowledge the data practices in our Privacy Policy.

Uneven office

Life in the city is showing signs of a somewhat comfortable new normal. Tourists have returned en masse, subways are sardine-packed and the majority of faces you see are maskless. Meanwhile, most industries have returned to their pre-pandemic levels of activity.

Less comfortable is the number of workers who are going back to the office. Despite growing demands from executives at major corporations like Disney and Google, only 42 percent of companies have required employees to return to the office full-time in the second quarter of 2023, according to the Flex Report, which collects data from more than 4,000 companies across the U.S.

Still, one aspect of New York City’s office market that’s quietly thriving, developers argue, is the premiere workplace landscape.

Across Manhattan, developers are forging ahead with earlier projects (filed before the time period covered by this ranking), including RXR’s 1,600-foot-tall tower at 175 Park Avenue that is slated to offer more than 2 million square feet of office space along with 500 hotel rooms, as well as Boston Properties’ nearly 1 million square foot office tower on the site of the MTA’s former headquarters.

“The occupancy rates around the Plaza District, particularly Park Avenue, are very, very strong,” said Hilary Spann, an executive with Boston Properties’ New York division, which placed fifth on the ranking thanks to its largest project at 343 Madison Avenue, just north of SL Green’s One Vanderbilt.

Commercial tenants looking for more than 100,000 square feet of space are struggling to find available properties with modern amenities worthy of bringing their employees back to the workplace, according to the developers TRD spoke with.

“We’re even hearing stories about tenants being displaced from their buildings by other tenants that are larger and expanding, and sort of having the smaller tenant scramble to find space,” Spann said.

Winners and losers

Looking ahead, developers predict that interest rate anxiety will be the driving factor impacting their prospective portfolios.

Uncertainty around interest rates compounds uncertainty in the market, developers argue. Real estate prices, which are based on the underlying spread of interest rates, have become increasingly difficult to predict in the turbulent market.

The answer to that problem is stability, but developers aren’t hopeful that’s coming anytime soon.

“That’s probably not going to happen in 2023,” said Spann. “It’s going to take a little while for everybody to digest the end of interest rate rises.”

But the lagging impact of interest rate hikes could create opportunities for deep-pocketed developers.

“The reality is, when interest rates rise like they have and loans expire, most owners who bought in the last 10 years have to pay down their loan in some capacity,” BEB Capital’s Brodsky said.

“I don’t believe that every owner is going to have the liquidity for those paydowns. And there’s going to be an opportunity for folks to enter those ownership groups at an optimal value that will lead to greater upside in the future.”

Vice chairman of Berkshire Hathaway says banks have a lot of bad commercial real estate loans

APR 30, 2023, 12:00 PM

By TRD Staff

Never one to be a shrinking violet, Charlie Munger has thoughts on the commercial real estate market, and none of them are particularly good.

“A lot of real estate isn’t so good any more,” Munger, the 99-year-old vice chairman of Berkshire Hathaway, told the Financial Times in an interview. “We have a lot of troubled office buildings, a lot of troubled shopping centers, a lot of troubled other properties. There’s a lot of agony out there.”

Banks are saddled with bad loans, as interest rates increase and property values fall, he told the outlet. Munger’s comments come at a time when Silicon Valley Bank and Signature Bank both collapsed last month, and the FDIC is seeking a buyer for San Francisco-based First Republic Bank, leading some to believe of a pending commercial real estate collapse.

“It’s not nearly as bad as it was in 2008,” he told the Times. “But trouble happens to banking just like trouble happens everywhere else. In the good times you get into bad habits. … When bad times come they lose too much.”

He noted that banks have tightened their commercial real estate lending, particularly over the past six months. The Times noted that Berkshire Hathaway hasn’t stepped into the current banking fray like it had during other shaky times.

“Berkshire has made some bank investments that worked out very well for us,” Munger said to the Times. “We’ve had some disappointment in banks, too. It’s not that damned easy to run a bank intelligently, there are a lot of temptations to do the wrong thing.”

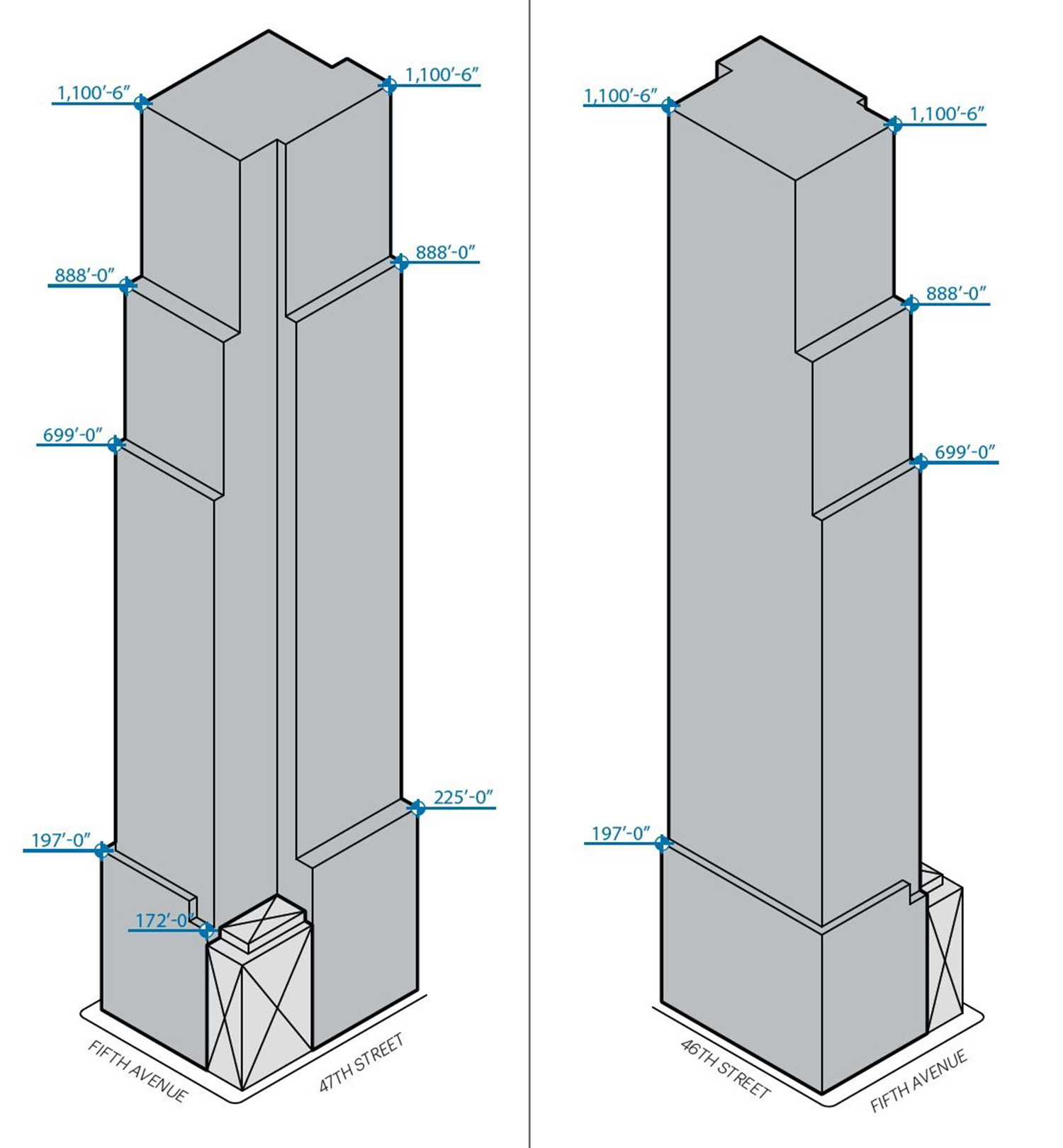

570 Fifth Avenue as an office (left) and mixed-use residence and hotel (right).

BY: MICHAEL YOUNG AND MATT PRUZNICK 8:00 AM ON APRIL 28, 2023

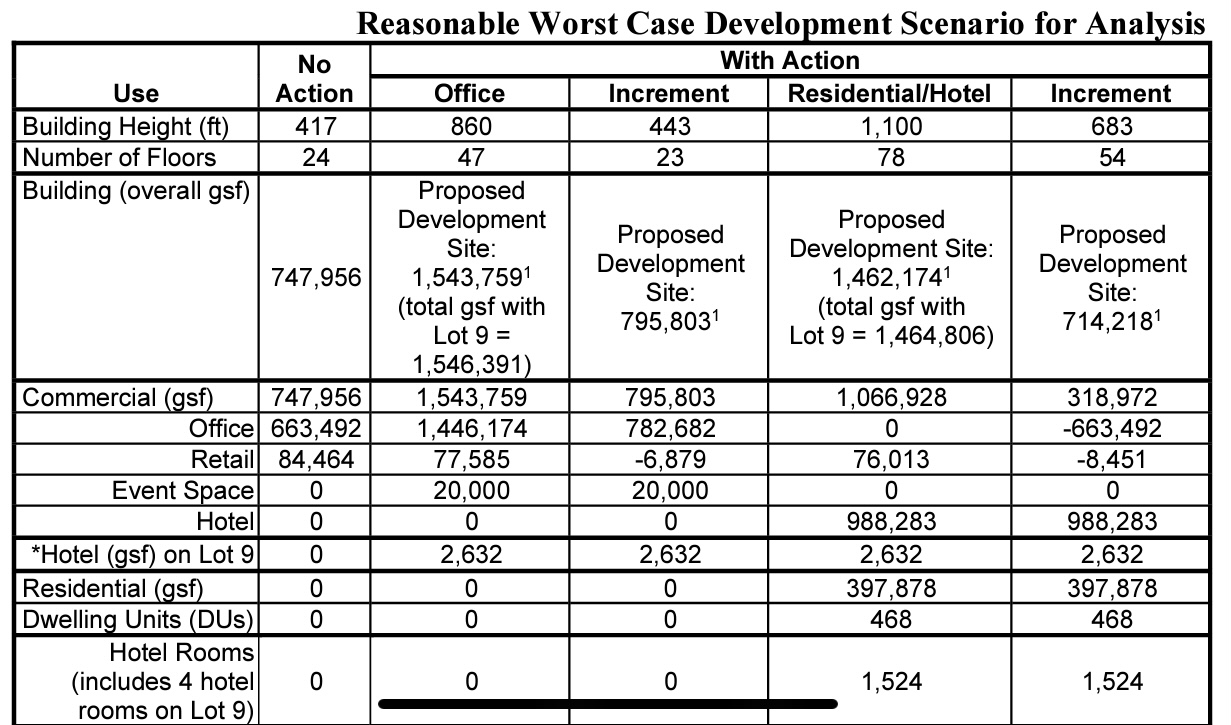

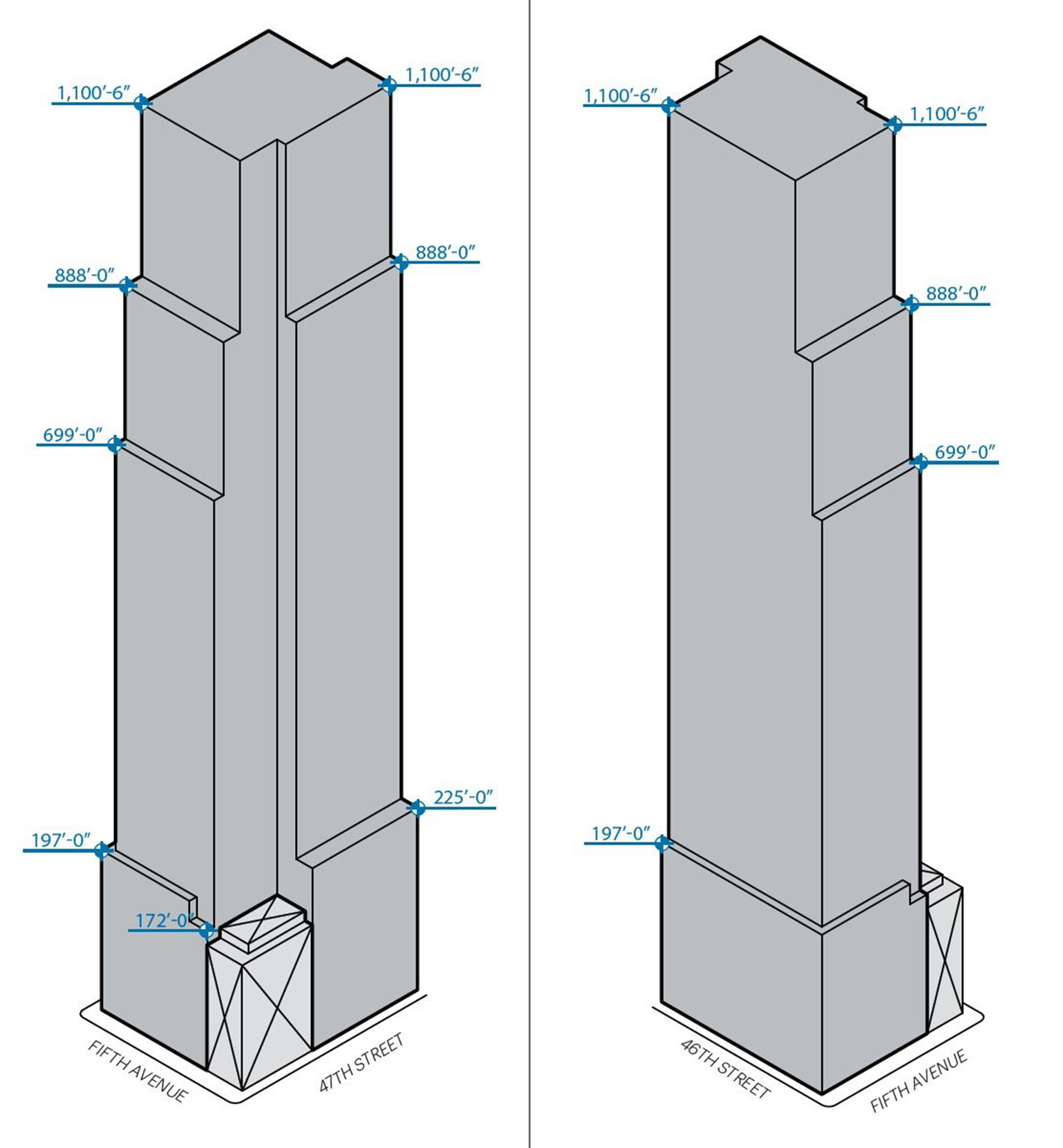

Demolition is complete at 570 Fifth Avenue, the site of a potential 1,101-foot mixed-use supertall in the Diamond District of Midtown, Manhattan. Developed by Extell, the project could either unfold as a 78-story, 1.4-million-square-foot hotel and condominium tower or as an 860-foot-tall, 47-story office skyscraper yielding more than 1.5 million square feet. ALBA Services was the demolition contractor for the property, which spans between West 46th and West 47th Streets.

Since our last update in December, the remaining rubble from the demolition of the plot’s final occupant has been cleared, and the property sits idly awaiting the start of excavation. It remains unclear when this activity will get underway.

570 Fifth Avenue. Photo by Michael Young

The 12-story, 172-foot-tall corner holdout at 576 Fifth Avenue will eventually be dwarfed by the massive scale of Extell’s future project.

The eye-catching glass curtain wall of Gary Barnett’s International Gem Tower is visible to the west of the site.

Photo by Michael Young

The following rendering of 570 Fifth Avenue’s multi-story podium shows the first two levels dedicated to retail space and a tall main entrance along Fifth Avenue. A landscaped terrace is depicted atop the podium setback.

The top floors of 570 Fifth Avenue as a supertall.

The upper portion of 570 Fifth Avenue will have a collection of relatively shallow setbacks, most of which are placed on the eastern elevation, while the back western profile will remain almost completely flat.

The chart below details each development scenario. The residential and hotel design will be Extell’s third project to surpass 1,000 feet in New York City and will become the second tallest skyscraper along Fifth Avenue after the Empire State Building.

YIMBY last reported that foundation work is expected to last roughly 12 months, followed by the rise of the superstructure for 28 months with a three-month overlap with the initial below-grade work. After that, interior work will last another 28 months with an overlap of 11 months with the previous stage in construction.

A completion date for 570 Fifth Avenue has yet to be officially confirmed, though speculative reports have put it around 2027 should construction begin this year.

Gowanus Green. Designed by Marvel Architects

Gowanus Green. Designed by Marvel Architects

520 Fifth Avenue. Rendering courtesy of Binyan Studios

520 Fifth Avenue. Rendering courtesy of Binyan Studios

570 Fifth Avenue as an office (left) and mixed-use residence and hotel (right).

570 Fifth Avenue as an office (left) and mixed-use residence and hotel (right).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}