Generous tenant-improvement packages left cash flows thin when remote work and higher interest rates hit

AUG 7, 2023, 7:00 AM

By

Rich Bockmann

As offices started transforming in the mid 2010s from drop ceilings and cheap carpet to resemble mid-century styled hotels packed with amenities like ping-pong tables and fully-stocked bars, the real estate team at insurance giant Prudential had an epiphany.

All the cash landlords were giving tenants to build out those pricey spaces was eating into the bottom line.

“It became clear to us that the dynamics of office had permanently changed,” said Lee Menifee, head of research for the Americas at PGIM Real Estate.

The writing was on the wall for PGIM and others who could see that offices would struggle. Around 2015 the insurer began shifting the bulk of its real estate portfolio away from workplaces and toward property types with better prospects, such as apartments and warehouses.

“Some investors started to sell down their office assets,” he added. “I think we were a little earlier.”

While the existential threat offices are dealing with now has largely been blamed on remote work and higher interest rates, the truth is that the sector had been struggling with disappointing returns for roughly a decade before Covid hit.

Had office buildings not seen their cash flows eaten away by those ever-climbing expenses, they arguably would have been in a better position to cope with the one-two punch of sinking demand and rising borrowing costs.

Offices in the country’s 20 largest central business districts saw returns underperform in all but two years since 2008, according to data from the National Council of Real Estate Investment Fiduciaries.

Part of this had to do with the outsized gains seen in areas like industrial and multifamily properties. But a driving factor was the escalating costs it took to attract tenants in the form of free rent and tenant improvement allowances.

Sign Up for the National Weekly Newsletter

SIGN UP

By signing up, you agree to TheRealDeal Terms of Use and acknowledge the data practices in our Privacy Policy.

Concessions like these typically tick up in soft markets when there’s more competition to land tenants. This time around, though, they became sticky as markets recovered following the Great Recession.

Office owners started dangling more sweeteners to lure companies to their buildings. Tenants began relocating offices more often than they had in the past, creating an incentive spiral that got out of hand.

“Long before the pandemic, we were seeing that tenants wanted more flexibility and highly-amenitized spaces, which resulted in office capital expenditure requirements increasing faster than rents,” said a spokesperson for Blackstone Group.

The firm, like PGIM, decided to reduce its focus on offices, which in 2007 made up roughly 60 percent of its portfolio. That share has shrunk to less than 2 percent today.

How significant are these costs to a building’s operations? When the total outlay for free-rent periods and tenant-improvement packages are factored in, it can be three to five years into a lease before a landlord starts to make money on the deal.

And the bad news for building owners is that those costs don’t seem to be softenting any time soon.

Tenant allowances went from about $67.50 in 2019 to more than $95 at the start of 2023, according to CBRE. Free rent went from roughly 7 months to more than 10.

And with interest rates going up, it’s going to cost even more to write those TI checks, according to CBRE’s Julie Whelan.

“It’s become much more expensive for landlords to give these allowances,” Whelan said.

Developers built the city up despite rising interest rates, empty offices and a major multifamily policy loss.

From left: Domain Companies’ Matt Schwartz, Joseph Chetrit, Extell Development’ s Gary Barnett and Taconic Partners’ Charles Bendit and Paul Pariser (Photo-illustration by Kevin Rebong/The Real Deal; photos via Getty Images, Domain Companies, Taconic Partners)

JUL 3, 2023, 7:00 AM

By Ellie Quilan Houghtaling

Research by Matthew Elo

Uncertainty reigns in real estate, but New York City developers are still reaching for the sky.

The city’s biggest builders have spent the past year shackled by rising interest rates, persistent supply-chain issues, a battered office market and a murky future for multifamily projects without the popular 421a tax break.

Despite all of this, developers came out of the year predicting gains in a down market and a cheery outlook for the city’s resilience as it continues to recover from the pandemic.

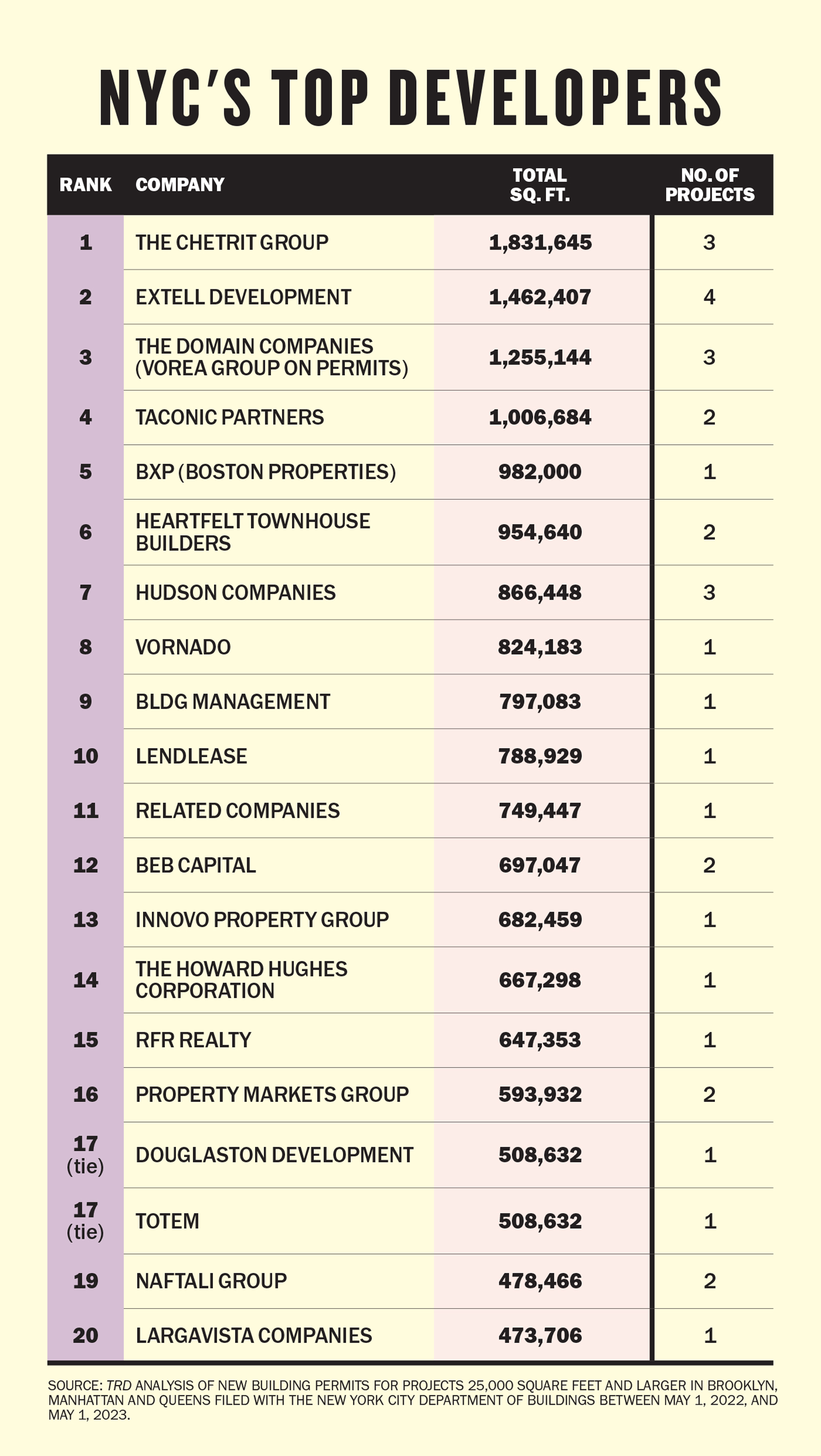

In the 12 months preceding May 1, the city’s 20 most active developers filed plans for 16.7 million square feet of new development — nearly a million more than in the previous year-long period.

To gain a clearer picture of which developers have the most skin in the game in the coming years, The Real Deal analyzed all new building filings submitted to the Department of Buildings between May 1, 2022, and May 1, 2023.

For the second year in a row, Moroccan émigré Joseph Chetrit’s eponymous firm topped the list, filing plans to develop just shy of 2 million square feet across three new projects. Its plans included the largest filing in the city: a 71-story mixed-use skyscraper with allotments for affordable housing on a Two Bridges development site that Chetrit Group bought from CIM Group and L+M Development Partners for $100 million in 2021.

Also included in the firm’s count is 100 West 37th Street in the Garment District, where Chetrit filed plans for a 360,000-square-foot, 68-story tower.

Gary Barnett’s Extell Development placed second, plotting out four new developments that combine for an estimated 1.5 million square feet. Extell’s major projects include 259 Clinton Street, a 421a-approved, 62-story tower just a block from Chetrit’s Two Bridges site. On the Upper East Side, Barnett’s firm filed more plans for a 30-story, 400,000-square-foot medical tower at 403 East 79th Street, also known as 1520 First Avenue.

Rounding out the top three was Domain Companies, which filed plans for nearly 1.3 million square feet across three multifamily projects. Those included a 500-unit complex at 2-33 50th Avenue in Long Island City and two Gowanus projects: a 360-unit, two-tower development at 420 Carroll Street and a 241-unit building at 545 Sackett Street.

Multifamily limbo

The end of 421a last summer created a host of challenges for developers. For those who managed to get foundations laid in time to qualify for the tax break, the 2026 construction deadline now looms large. Some worksites across the city could face supply-chain hiccups that could have a devastating effect.

“I think it’s at the point now where the deadline is getting a little bit close for comfort,” said Domain Companies co-founder Matt Schwartz.

Hopes fluttered and then faltered over Gov. Kathy Hochul’s housing plan, which sought to address some of these challenges but failed to garner enough support from state lawmakers. Entering summer without an immediate replacement for 421a in the cards, developers say they’re focusing on projects already in their portfolio rather than reaching for the horizon.

“If we don’t have something in the pipeline and advancing, we’re generally stuck in a kind of wait-and-see mode. Which is unfortunate, given where we are,” Schwartz said. “We’re very bullish on New York, but the affordability crisis is a real threat.”

“Those that aren’t prepared to proceed to hit the deadline are going to be hurt,” added Lee Brodsky, CEO of BEB Capital, which placed 12th on the list with nearly 700,000 square feet across two projects.

Developers who find themselves unable to meet the deadline will have to find other solutions for their overpriced land, with possible pivots toward condos or luxury rentals.

Sign Up for the National Weekly Newsletter

SIGN UP

By signing up, you agree to TheRealDeal Terms of Use and acknowledge the data practices in our Privacy Policy.

Uneven office

Life in the city is showing signs of a somewhat comfortable new normal. Tourists have returned en masse, subways are sardine-packed and the majority of faces you see are maskless. Meanwhile, most industries have returned to their pre-pandemic levels of activity.

Less comfortable is the number of workers who are going back to the office. Despite growing demands from executives at major corporations like Disney and Google, only 42 percent of companies have required employees to return to the office full-time in the second quarter of 2023, according to the Flex Report, which collects data from more than 4,000 companies across the U.S.

Still, one aspect of New York City’s office market that’s quietly thriving, developers argue, is the premiere workplace landscape.

Across Manhattan, developers are forging ahead with earlier projects (filed before the time period covered by this ranking), including RXR’s 1,600-foot-tall tower at 175 Park Avenue that is slated to offer more than 2 million square feet of office space along with 500 hotel rooms, as well as Boston Properties’ nearly 1 million square foot office tower on the site of the MTA’s former headquarters.

“The occupancy rates around the Plaza District, particularly Park Avenue, are very, very strong,” said Hilary Spann, an executive with Boston Properties’ New York division, which placed fifth on the ranking thanks to its largest project at 343 Madison Avenue, just north of SL Green’s One Vanderbilt.

Commercial tenants looking for more than 100,000 square feet of space are struggling to find available properties with modern amenities worthy of bringing their employees back to the workplace, according to the developers TRD spoke with.

“We’re even hearing stories about tenants being displaced from their buildings by other tenants that are larger and expanding, and sort of having the smaller tenant scramble to find space,” Spann said.

Winners and losers

Looking ahead, developers predict that interest rate anxiety will be the driving factor impacting their prospective portfolios.

Uncertainty around interest rates compounds uncertainty in the market, developers argue. Real estate prices, which are based on the underlying spread of interest rates, have become increasingly difficult to predict in the turbulent market.

The answer to that problem is stability, but developers aren’t hopeful that’s coming anytime soon.

“That’s probably not going to happen in 2023,” said Spann. “It’s going to take a little while for everybody to digest the end of interest rate rises.”

But the lagging impact of interest rate hikes could create opportunities for deep-pocketed developers.

“The reality is, when interest rates rise like they have and loans expire, most owners who bought in the last 10 years have to pay down their loan in some capacity,” BEB Capital’s Brodsky said.

“I don’t believe that every owner is going to have the liquidity for those paydowns. And there’s going to be an opportunity for folks to enter those ownership groups at an optimal value that will lead to greater upside in the future.”

Vice chairman of Berkshire Hathaway says banks have a lot of bad commercial real estate loans

APR 30, 2023, 12:00 PM

By TRD Staff

Never one to be a shrinking violet, Charlie Munger has thoughts on the commercial real estate market, and none of them are particularly good.

“A lot of real estate isn’t so good any more,” Munger, the 99-year-old vice chairman of Berkshire Hathaway, told the Financial Times in an interview. “We have a lot of troubled office buildings, a lot of troubled shopping centers, a lot of troubled other properties. There’s a lot of agony out there.”

Banks are saddled with bad loans, as interest rates increase and property values fall, he told the outlet. Munger’s comments come at a time when Silicon Valley Bank and Signature Bank both collapsed last month, and the FDIC is seeking a buyer for San Francisco-based First Republic Bank, leading some to believe of a pending commercial real estate collapse.

“It’s not nearly as bad as it was in 2008,” he told the Times. “But trouble happens to banking just like trouble happens everywhere else. In the good times you get into bad habits. … When bad times come they lose too much.”

He noted that banks have tightened their commercial real estate lending, particularly over the past six months. The Times noted that Berkshire Hathaway hasn’t stepped into the current banking fray like it had during other shaky times.

“Berkshire has made some bank investments that worked out very well for us,” Munger said to the Times. “We’ve had some disappointment in banks, too. It’s not that damned easy to run a bank intelligently, there are a lot of temptations to do the wrong thing.”

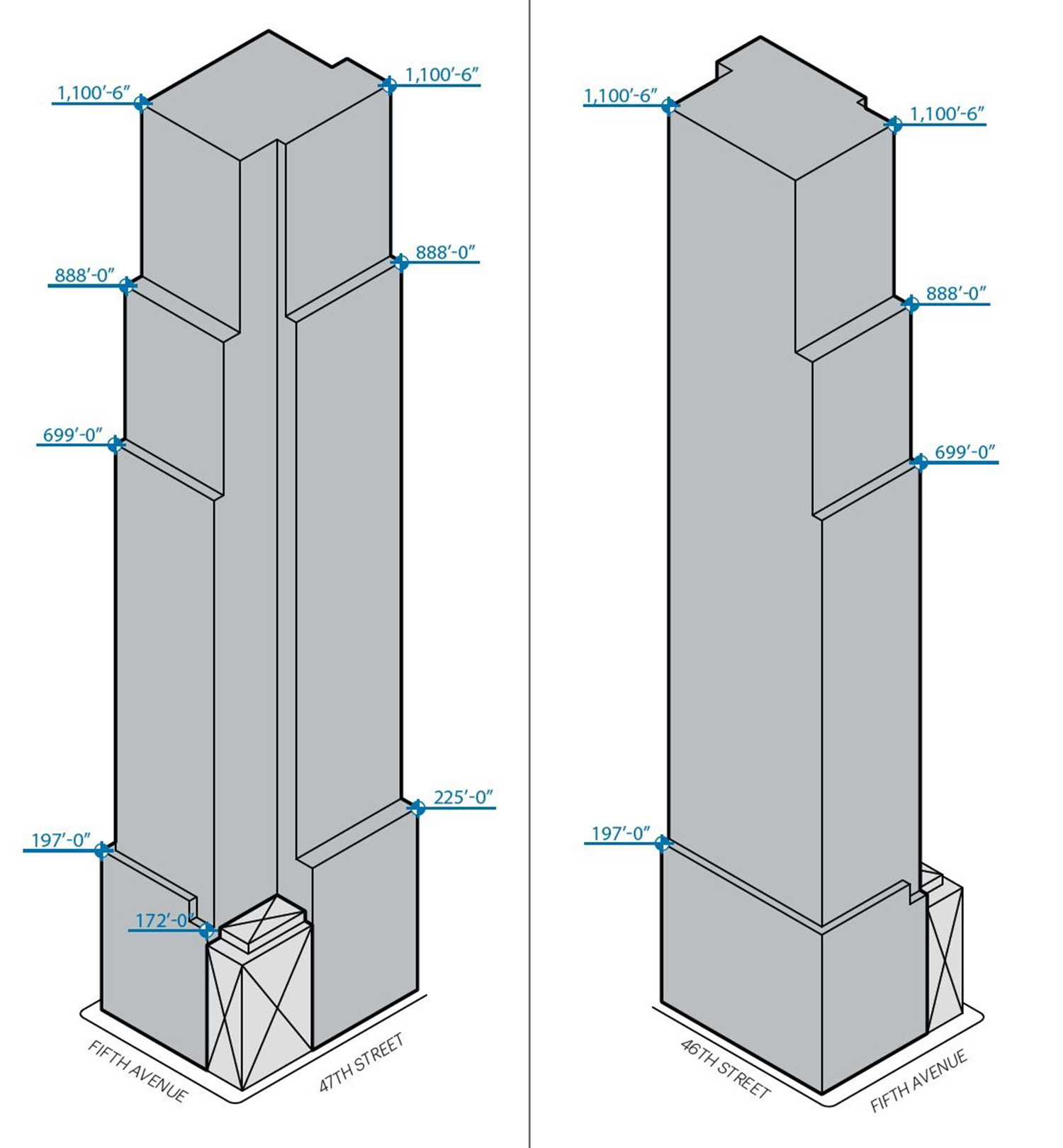

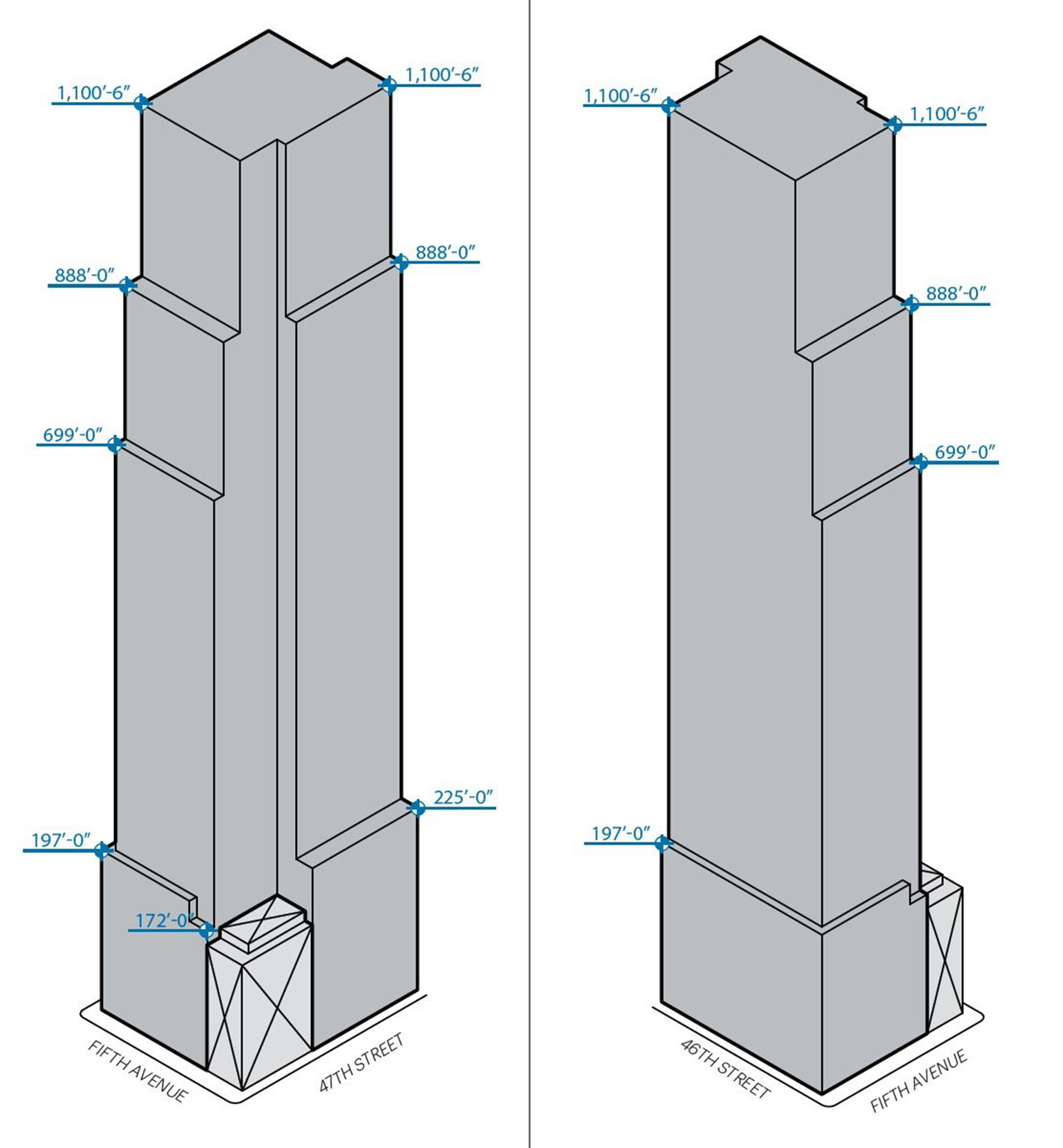

570 Fifth Avenue as an office (left) and mixed-use residence and hotel (right).

BY: MICHAEL YOUNG AND MATT PRUZNICK 8:00 AM ON APRIL 28, 2023

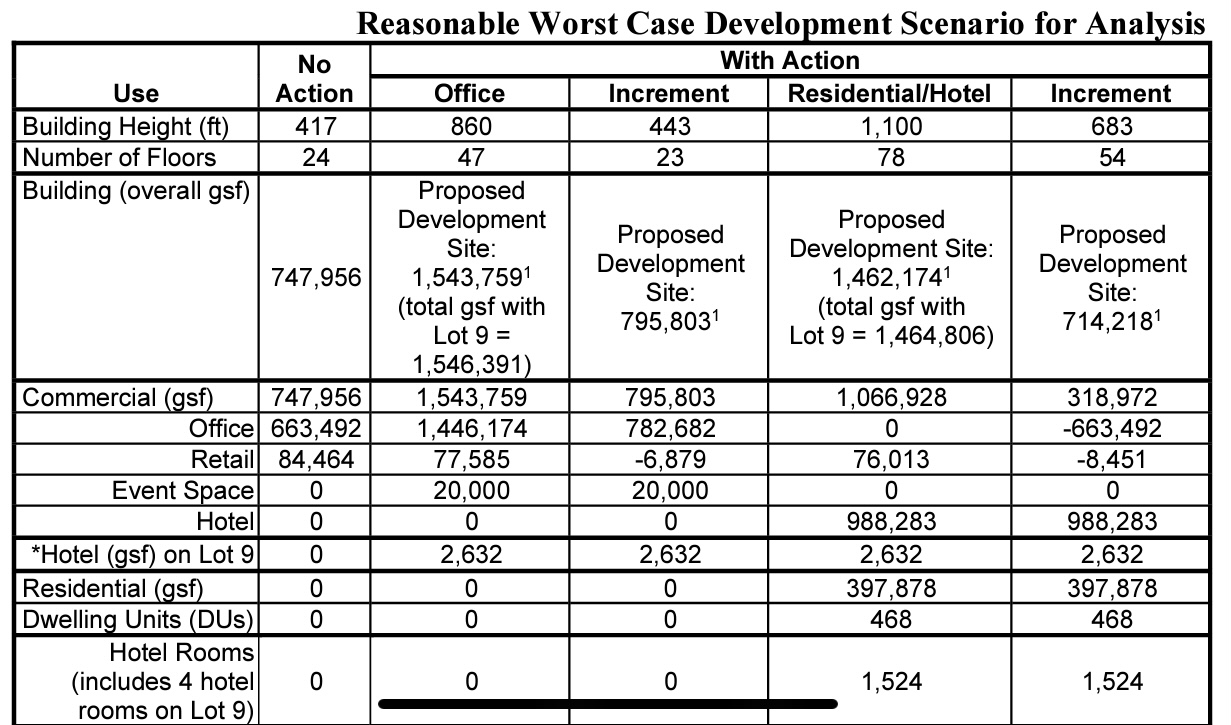

Demolition is complete at 570 Fifth Avenue, the site of a potential 1,101-foot mixed-use supertall in the Diamond District of Midtown, Manhattan. Developed by Extell, the project could either unfold as a 78-story, 1.4-million-square-foot hotel and condominium tower or as an 860-foot-tall, 47-story office skyscraper yielding more than 1.5 million square feet. ALBA Services was the demolition contractor for the property, which spans between West 46th and West 47th Streets.

Since our last update in December, the remaining rubble from the demolition of the plot’s final occupant has been cleared, and the property sits idly awaiting the start of excavation. It remains unclear when this activity will get underway.

570 Fifth Avenue. Photo by Michael Young

The 12-story, 172-foot-tall corner holdout at 576 Fifth Avenue will eventually be dwarfed by the massive scale of Extell’s future project.

The eye-catching glass curtain wall of Gary Barnett’s International Gem Tower is visible to the west of the site.

Photo by Michael Young

The following rendering of 570 Fifth Avenue’s multi-story podium shows the first two levels dedicated to retail space and a tall main entrance along Fifth Avenue. A landscaped terrace is depicted atop the podium setback.

The top floors of 570 Fifth Avenue as a supertall.

The upper portion of 570 Fifth Avenue will have a collection of relatively shallow setbacks, most of which are placed on the eastern elevation, while the back western profile will remain almost completely flat.

The chart below details each development scenario. The residential and hotel design will be Extell’s third project to surpass 1,000 feet in New York City and will become the second tallest skyscraper along Fifth Avenue after the Empire State Building.

YIMBY last reported that foundation work is expected to last roughly 12 months, followed by the rise of the superstructure for 28 months with a three-month overlap with the initial below-grade work. After that, interior work will last another 28 months with an overlap of 11 months with the previous stage in construction.

A completion date for 570 Fifth Avenue has yet to be officially confirmed, though speculative reports have put it around 2027 should construction begin this year.

The bill, introduced by Sen. Gary Winfield (D-New Haven), would cap increases between landlords and tenants as well as agreements between tenants. Owner-occupied properties with one to four units would be excluded.

State law only provides good-cause-eviction protections — preventing no-fault of retaliatory evictions following tenant complaints about maintenance — to people over the age of 62 and those living with disabilities, the outlet reported. The law prevents landlords from issuing no-fault evictions or retaliatory evictions following a tenant’s complaints about maintenance issues.

Tenant advocacy groups are supporting the measure in light of rents soaring an average of 20 percent in the past two years, according to CT Insider.

“This is an important and historical time in our world, where we have real opportunities for change,” Greta Blau, a Hamden Tenant Union leader, told the outlet. “Ending no-cause eviction will ensure that many more Connecticut residents will have housing security for years to come.”

Haberfeld said there are already protections in place for tenants and capping rent increases will lead to landlords cutting corners elsewhere.

“Landlords that don’t fix their apartments and keep them up, that is definitely not okay. But we already have something in place to combat that and that’s code enforcement,” he told WFSB.

Nationwide, advocates have called for greater tenant protections amid the pandemic.

The new seven-member board, to launch by July, will oversee enforcement of the city’s rent control law and offer tenants and landlords a place to resolve disputes outside of court.

There were 351 new building filings in New York City in the third quarter, down 17 percent from the second quarter and 28 percent year-over-year, according to a report from the Real Estate Board of New York.

The drop is in part because the 421a property tax break for multifamily development in the city expired June 15, which triggered a rush of filings. The 689 in the first quarter were the most in a quarter since 2014, which, not coincidentally, was just before the previous version of 421a expired.

A drought followed the 2014 surge, and now history is repeating itself. Developers have all but stopped trying to put together investors to pursue rental projects that cannot get the 35-year property tax break. Condo projects were largely excluded from the most recent iteration of 421a.

Rising interest rates have also contributed to the decline, as financing projects of all kinds became more challenging for developers.

But the impact of 421a’s expiration is clear when comparing the slowdown in filings for rental projects to the overall drop in new-building filings. The quarter-over-quarter falloff in rental filings was 62 percent, nearly four times the quarterly decline overall. Only 78 rental projects were filed in the quarter, half as many as in the same period last year.

Those 78 projects are proposed to have 3,346 units, down 46 percent year-over-year and the smallest quarterly number in a decade — since the slump that followed the 2008 financial crisis.

Rental projects in much of the city became dependent on 421a over several decades. Progressives let the tax break lapse, believing it forgave too much property tax for too little affordability. Some predict it will be several years before it is replaced, although an abatement still exists for co-ops and condos.

Experts have estimated the city needs to build approximately 560,000 units by 2030 to catch up with demand for housing in the city.

The spikes in 2014 and 2022 coincide with expirations of 421a. (REBNY)

“We face a severe housing shortage that is only getting worse and hopefully these sobering findings will encourage stakeholders to advance policies that facilitate more of the development and construction activity that our city needs,” REBNY’s Zachary Steinberg said in a statement.

More than a third of the quarter’s proposed multifamily units were in Brooklyn, while the Bronx and Queens both grabbed larger shares than in the second quarter.

Multifamily construction was quiet in Manhattan and Staten Island, though, which combined for only 10 multifamily developments. However, Boston Properties’ 982,000-square-foot project at 343 Madison Avenue in Manhattan was the largest filing of the quarter.

Third-quarter filings accounted for 6.4 million square feet, a drop of 57 percent from the previous quarter and 20 percent year-over-year.

JPMorgan Chase, Deutsche Bank, Barclays exploring debt sales

National /

November 11, 2022 04:00 PM

TRD Staff

JPMorgan Chase’s Jamie Dimon, Deutsche Bank’s Christian Sewing and Barclays’ Nigel Higgins (JPMorgan Chase, Deutsche Bank, Barclays, Getty)

Is the other shoe about to drop on commercial real estate?

Just in case it is, prominent lenders for commercial properties, especially offices, are exploring sales of their loans in cities with low demand, including New York, Bloomberg reported. JPMorgan Chase, Deutsche Bank and Barclays are among them.

In a sign of how motivated lenders are to offload debt, some are offering discounts ranging from 3 percent to 25 percent. Many of the talks around selling debt have been held behind closed doors, and debt deals are largely being kept out of the public eye.

The risks lenders face include that the properties secured by their loans will not generate enough revenue for their owners to pay the debt service, and the assets’ value will fall below the loan balance.

“Office in particular is a dirty word for lenders,” Jeff Kaplan of Meadow Partners told the publication.

Selling loans is a normal course of business for banks. What’s not, however, is the struggle they are having finding buyers. Hence the discounts.

Lenders issued $316 billion in commercial loans across the country in the first half the year, according to the Federal Reserve. But rising interest rates and distress for certain commercial property types has lenders reversing course.

Many have become hesitant to originate debt, fearing rising rates and inflation will reduce the value of those loans in the future. Some commercial real estate players are taking out variable-rate loans rather than lock in fixed-rate loans at high interest rates.

Commercial lenders are responding to declining property prices across the sector. Commercial prices are down 13 percent from a May peak, according to the Green Street Commercial Property Price Index. Shopping malls have taken the biggest hit with a 23 percent drop, but even industrial prices are down 17 percent since May.

In the long term, office landlords may have it the worst. A study by NYU’s Arpit Gupta and Columbia University’s Vrinda Mittal and Stijn Van Nieuwerburgh estimated that by 2029, New York City’s office stock will fall in value by 28 percent, or $49 billion.

The major cities of the Northeast have faced a paradox of high demand and low overall growth. Businesses still want to locate, for instance, in New York City, and people still want to move there, but a combo of taxes, high home prices and quality-of-life problems often discourage moving to the city itself. But across the river a different city—and a general area—has embraced urban growth where New York City eschewes it. Jersey City and others along the North Jersey shore have grown at a faster rate this last decade, creating what could be thought of as the 6th borough.

This starts with permits; Jersey City and neighboring cities build substantially more housing than most of the New York metro area at large. According to the Citizen’s Budget Commission, Hudson County overall permits well over double the rate of housing that New York City does (51 units/10ks residents vs. 22 units/10k residents). For this reason Hudson County is growing faster than New York City (7% vs 3% from 2011-2020) and the percentage growth rate since then is a whopping 18% for Jersey City.

Many renters move to Jersey City; it was one of the top 10 destinations for renters in the U.S. This includes New York City renters in particular, suggesting they can find a similar lifestyle across the river. Jersey City does have a high average rent price, at $3,821 for a 2-bedroom apartment, but it’s cheaper than New York City’s overall average of $4,927. Furthermore, the money stretches further along the west side of the Hudson River. As a local realtor stated: “In Jersey City you can purchase a brand-new construction condo with three bedrooms, two baths, private outdoor space, parking, laundry and roof deck with NYC views for less than $1 million. In many parts of New York City, this same condo would be upward of $2 to 3 million.”

What’s perhaps more notable are rents around Jersey City. Union City, NJ, is one of the densest municipalities in America. The average rent per 1-bedroom apartment there is $1,700 and the median household income is below $50,000. In Bushwick, a Brooklyn neighborhood noted for its gentrification, median incomes are similar but the average rent is $2,700. From 2014 to 2022, rents increased by 32% in Union City, but this was 6% lower than Bushwick’s rate. To be sure, lower home prices typically run along a gradient the further one searches from a central area. But Jersey City, where the finance industry grew 500% between 1993 and the present day, is arguably central in its own right. And it’s likely that high density construction there has made both Jersey City and neighboring suburbs like Union City more affordable.

New York’s housing production is anemic relative to demand, both in the city and surrounding non-Jersey suburbs. Notes the Citizen’s Budget Commission: “counties like Westchester, Rockland, Nassau, and Suffolk have some of the lowest housing production rates in the country.” Despite being known for density more than any other U.S. city, New York has in fact downzoned in recent decades. A 2010 NYU study found that out of 180,000 parcels, “14 percent had been upzoned, 23 percent downzoned, and 63 percent had not had their development capacity changed by more than 10 percent” the prior decade, reported Politico.

Jersey City, by contrast, encourages high-rise construction. According to SkyscraperCenter, the city is the 10th “tallest” in the United States (and 13th in North America). While Manhattan is famous for its skyscrapers, this is mostly a legacy from more permissive past eras, and now anti-height NIMBYismis common. By contrast, Jersey City has allowed a whole new skyline, with 35 of its 43 tallest towers getting built since 2000.

Jersey City also embraces other urbanist bona fides, often with a free-market twist. Several of the private ferries serving New York City stop along the Jersey City waterfront, providing connections to Midtown and Lower Manhattan, as does the PATH train, which provides 24/7 service, and a light rail line to points throughout the North Jersey suburbs. Interestingly, Hudson County also embraces private bus transit, with jitneys making trips throughout the day within North Jersey and to Manhattan, charging cheap fares. The city is also among those which have launched a subsidized microtransit service, supplementing other transit services.

But Jersey City is not just a bedroom community for New York commuters; jobs in the city itself have grown. Numerous financial district firms have opened satellite offices in the city dating back to the early 1990s. Tech interest and employment is also growing, with one software firm leasing tens of thousands of square feet even amid the pandemic.

Jersey City—and the larger Hudson County urban oasis that includes Union City, Hoboken, Bayonne and more—could make its case as a proverbial “6th Borough” of New York City. While it could always do more to liberalize its land use and other fiscal policies, it has done a much better job than New York City proper of accommodating the region’s population demands. As a result it has become a very different city the last decade, while much of the rest of the region stagnates under an anti-growth mindset.

The Albanese Organization is planning 670 luxury apartments at 286 Coles St. in Jersey City, as depicted in this rendering by Marchetto Higgins Stieve Architects — Courtesy: Grid Real Estate

By Joshua Burd

A developer has acquired nearly two acres in Jersey City with plans to build 670 luxury apartments on the property, in a recently completed deal by Grid Real Estate.

The Albanese Organization, a Garden City, New York-based firm, paid $70 million for the 1.83-acre parcel at 286 Coles St., where it joins a growing list of builders involved in revitalizing a neighborhood near the Hoboken border and just west of the Holland Tunnel. The firm reportedly plans to break ground early next year, with approvals in place and plans calling for the project to span the entire block between 16th and 17 streets.

Grid’s Bob Antonicello and Bobby Antonicello Jr. represented Albanese in the deal, noting that Hoboken Brownstone Co. previously owned the land. Eugene Paolino and Jeff Rich of Genova Burns LLCwere also involved in the transaction.

“We are excited to play a part in the redevelopment of 286 Coles Street,” Bob Antonicello said. “The Albanese team has designed a world-class mixed-use property that will be a welcomed addition to the downtown/Hoboken residential market.”

Part of a large redevelopment area, the Albanese project would rise alongside thousands of other units that have helped transformed the longtime industrial neighborhood at the northern end of Jersey Avenue. The area is also home to the recently opened Coles Park as a result of a $2.5 million investment by Manhattan Building Co., which has delivered nearly 800 apartments in the neighborhood since 2013 and had another 350 under construction when it broke ground on the park in late 2019.

Albanese, for its part, has other projects in Jersey City, including the Hendrix, a 482-unit property at 184 Morgan St., and the proposed 6th Street Embankment project.

Construction is rising on One Madison Avenue, a 27-story commercial expansion in the Flatiron District. Designed by Kohn Pedersen Fox and developed by SL Green, the National Pension Service of Korea, and Hines, the project involves the gut renovation and expansion of a former eight-story structure and will yield 1.4 million square feet of office space. AECOM Tishman is the general contractor for the property, which occupies a full block bound by East 23rd and 24th Streets and Madison Avenue and Park Avenue South.

At the time of our last update in mid-June, the core for the tower expansion was just beginning to rise above the gutted podium. Since then, the reinforced concrete volume has risen steadily as work on the surrounding steel frame has begun to take shape. Based on the pace of progress, the core should top out before the end of the year, with the framing following shortly behind.

O

One Madison Avenue. Photo by Michael Young

Two tower cranes are busily hoisting steel into place for the tower’s frame. Nearly all of the new windows are in place on the lower floors, arranged in a grid of vertical columns.

One Madison Avenue. Photo by Michael Young

The new tower will yield 530,000 square feet with floor plates spanning up to 35,000 square feet each. The glass curtain wall will provide occupants with abundant natural light and panoramic views of Madison Square Park, the Flatiron Building, and the surrounding neighborhood. The tenth and 11th floors will feature 22-foot ceiling spans and provide access to an open-air rooftop deck. Additional outdoor terraces will sit atop the podium between Madison Avenue and Park Avenue South.

Office amenities at One Madison Avenue include a 15,000-square-foot artisanal food market, a 9,000-square-foot tenant lounge, a three-level fitness center, bicycle storage, and a 13,000-square-foot high-tech event space with a capacity of 800 people. The closest subways from the property are the R and W trains at the 23rd Street station to the west along Broadway, and the local 6 train to the west along Park Avenue South. It was last announced that IBM has signed on as the anchor tenant with plans to occupy 328,000 square feet across five floors.

One Madison Avenue is slated for completion by the end of November 2023.

570 Fifth Avenue as an office (left) and mixed-use residence and hotel (right).

570 Fifth Avenue as an office (left) and mixed-use residence and hotel (right).

Rendering of One Madison Avenue Expansion. Designed by Kohn Pedersen Fox

Rendering of One Madison Avenue Expansion. Designed by Kohn Pedersen Fox

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}